Managing grants from federal agencies is crucial especially if you expend $750K or more in one given year. Are there basic principles to follow when managing grants? Thankfully there is. Generally speaking grant managers should be knowledgeable in the grant’s specific compliance requirements and the basic principles to managing a grant of federal funds. There is much information when it comes to compliance requirements with the federal government, and each grant depending on its nature and size will have different requirements, but there are basic guidelines for these grants. Some of these basic guidelines are the basis for this discussion.

Federal grants requires for management to practice sound management principles as it pertains to the grant award. There are 12 compliance requirements that just about each grant manager needs to follow. These 12 include the following:

- Allowed / unallowed activities

- Allowable costs and cost principles

- Cash management

- Eligibility

- Equipment and real property management

- Matching, level of effort, and earmarking

- Period of performance

- Procurement and suspension and debarment

- Program income

- Reporting

- Sub-recipient monitoring

- Special tests and provisions

First, we’ll define each of the 12 compliance requirements, and then we’ll cover compliance requirements when it comes to Financial Management Systems, procurement practices, equipment and real property procedures, financial reporting, and retention requirements.

- Activities Allowed or Unallowed – Speaks to which activities can or cannot be funded under the program. Costs related to unallowed activities need to be funded by the general fund

- Allowable costs and cost principles – This relates to which expenditures can be applied against the federal grant funds and these principles are found in OMB cost principles in the Uniform Guidance Subpart E . Indirect costs computation is also included in this compliance requirement.

- Cash Management – These are the procedures and policies of the entity to comply with cash management requirements of the grant

- Eligibility – This determines the individuals, groups of individuals, or subrecipients that can participate in the federal award program

- Equipment and Real Property Management – It requires a process to use, manage, and dispose the equipment/real property

- Matching, Level of Effort, and Earmarking – At times, the grant will match a certain amount dollar for dollar for a specific program or project. Level of effort speaks to the level of supplementing the program/project. Earmarking speaks to the minimum or maximum amount that must be used for specific program activities.

- Period of Performance – The time frame of the grant, when can it start funding , when does the funding end, etc

- Procurement , suspension, and debarment – This speaks to the policies and procedures used for procurements (payments) and the policies and procedures to include/exclude

- Program Income – Any income generated directly from an activity associated with the grant program or project

- Reporting – The reports include financial, performance, and special reports used to monitor the grantee and its operations

- Subrecipient Monitoring – The responsibilities of the entity that passes through the grant funds to subrecipients

- Special Test and Provisions – These are unique to the program and found in federal statutes, regulations, and the terms of the federal award.

RISK ASSESSMENT

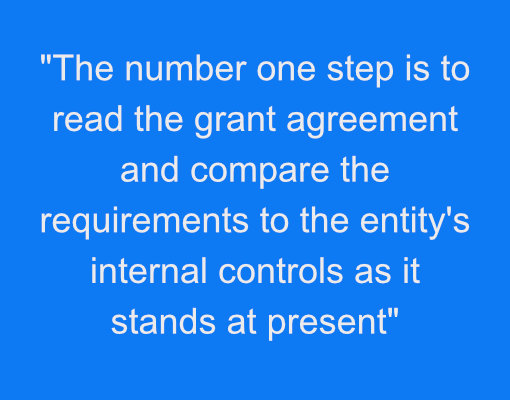

The entity receiving the grant awards should assess the risk or the likelihood that the entity doesn’t have the ability to comply with the grant agreement and its requirements. How does it assess the risk? The number one step is to read the grant agreement and compare the requirements to the entity’s internal control structure as it stands at present. Will the entity controls prevent fraud? Will it find personnel mistakes? Does the entity have the ability to submit reports on a timely basis and account for its revenues and expenditures? These are just a few examples of what the entity can do to ascertain its risk as to whether it has the ability to comply with the requirements. The entity also needs to be aware of its risk tolerance. How much risk is the entity willing to take on before a new procedure or policy needs to be created. When assessing the risk tolerance, it’s a good practice to perform a cost benefit analysis. At what point is the risk high enough to merit a change in the internal control system.

FINANCIAL MANAGEMENT SYSTEM

Management will need a financial management system to comply with the administrative requirements of the award. The federal government will ask for reports ascertaining whether or not you have complied with the grant requirements. It’s a good idea to have a financial management system. The financial management system must have the ability to provide the following:

- Identify revenues and expenditures related to the federal award including the CFDA title and number, federal award id, year, name of agency, and name of pass-through entity, if any

- Accurate, current complete disclosures of financial results

- Records that identify adequately the source and application of funds (make sure vendor invoices and other documentation reconcile to your books. Document the authorization of the revenues and expenditures

- Effective controls over and accountability for all funds, property, and other assets.

- Compare actual results to budget

- Procedures regarding payments of federal awards

- Procedures for determining the allowability of costs

Although you don’t necessarily need everything to be in a computer system or software, utilizing technology is the most efficient way to comply with these requirements. At the end of the day (so to speak), make sure the accounting system will use different classes or divisions to separate the grant award revenues and expenditures to the revenues and expenditures not relating to the award. The federal government does not require a certain type of software but does specify the financial management system needs to provide the information shown above. A sound financial management system keeps the entity organized and with sound internal controls provides the entity with the confidence the financial reports are accurate.

PROCUREMENT PRACTICES

Depending on the type of grant, the award will be dependent on different variables. For example, some require a reimbursement rather than advanced payments. Some may require the entity to perform a certain tasks or project prior to receiving the funds. At times, you may be required to submit additional reports. Make sure to read the grant agreement to understand how your entity will receive the grant award.

There are certain requirements when working with vendors regarding the project or program. Review your grant agreement first as the following scenarios are general requirements.

Micro-Purchase – If the total dollar amount doesn’t exceed $3,000 ($2,000 for construction projects subject to Davis-Bacon Act), no soliciting competitive quotes are needed or mandatory.

Small Purchase Procedures – These are for securing services, supplies, and other property that do not cost more than the Simplified Acquisition Threshold (SAT) of $150K. If the small purchase procedures are used, price or rate quotations must be obtained from many qualified sources.

Sealed Bids (Formal Advertising) – Bids are publicly solicited, and a firm fixed price contract is awarded to the responsible bidder whose bid, conforming with all the material terms and conditions of the RFP, is the lowest price.

Competitive Proposals – These are generally used when the Sealed Bids practice is not appropriate

Noncompetitive Proposals – This can be done if the following circumstances apply:

- Service only available from one source

- There’s an emergency and a bid is not appropriate

- The grant agreement authorizes non-competitive bids

- After many bids, the competition is determined not skilled enough to perform the tasks or project

Other Practices – Make sure you take steps to include small and minority businesses, women’s business enterprises, and labor surplus area firms are used when possible.

If the purchase price exceeds $150K, you’ll need to perform analysis of cost and price.

Contract Provisions – When a contract exceeds the SAT limit, the following information needs to be in the contract: Administrative, contractual, or legal remedies for contractor violations of contract terms. When contracts in excess of $10K, they must address termination for cause and for convenience. Also, make sure you have an “Equal Opportunity” clause in the contracts.

These are general requirements that depending on the situation must be followed. As mentioned previously, to review specific requirements, always refer to the grant agreement. Ensure your procurement procedures include the requirements of the grant.

SAFEGUARDING EQUIPMENT

There are certain requirements when grant funds purchase equipment or real property. The standards state the entity must have insurance coverage for real property and equipment.

Real Property – In addition to the insurance coverage, the entity must use the real property for the originally authorized purpose. Furthermore, if the entity no longer needs to use the real property for the original authorized purpose, it will need to obtain instructions from the federal awarding agency for the next steps. Either (1) the entity will compensate the federal agency in exchange for the real property, (2) Sell the property and compensate the federal awarding agency, or (3) transfer the title to the federal awarding agency or to a 3rd party designated/approved by the federal awarding agency.

Its crucial that the entity keeps track of the intended use of the equipment and contact the federal awarding agency if the intended use changes or the real property is disposed (sold or otherwise).

Federally Owned and Except Property – You must submit an inventory listing of all federally owned property in your possession. The federal government has full custody and if it is determined the property is no longer needed, it will dispose the property to the federal disposal authority.

Equipment – The equipment must be used for its intended and authorized purpose. If the there is no need to use the equipment for the originally intended purpose, then the entity is allowed to use the equipment for other federally awarded programs/projects. If the equipment is not used for any federally awarded programs/projects, you can use the equipment for regular operations.

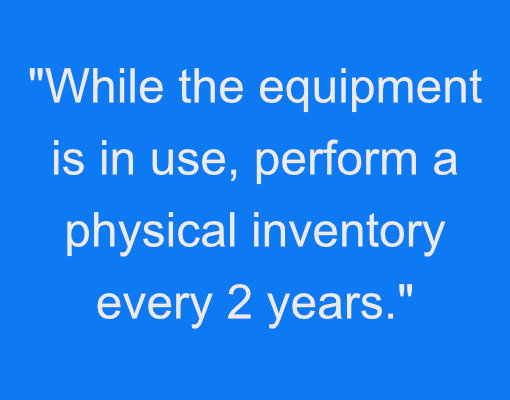

Other Safeguards – While the equipment is in use, perform a physical inventory at minimum every 2 years. Also, make sure the equipment is safe and controls are in place to keep it from getting stolen, damaged, or lost. And if in the occurrence the equipment is lost, damaged, or stolen, there must be an investigation.

Maintenance procedures must be developed and performed to ensure the equipment is kept in good condition. When it comes to selling the equipment, the federal government requires you to establish procedures to ensure you receive the highest possible return.

There are certain rules to dispose of equipment. If the fair market value is $5,000 or less it may be retained, sold, or disposed of without any communication to the federal awarding agency. If the selling price is greater than $5,000 then you’ll need to communicate to the federally awarding agency and they’ll require a portion of the proceeds of the sale (gain on sale). The portion would be the gain on sale multiplied by their share of the amount awarded. For example, if they awarded 50% of the total cost, then 50% of the gain on sale would be sent to the federally awarding agency.

FINANCIAL REPORTING

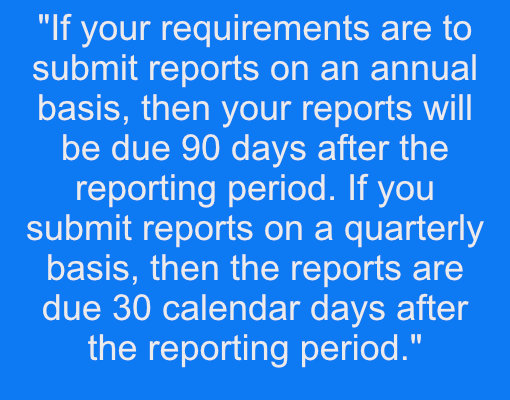

Generally speaking, your financial reporting requirements won’t be any less than once a year and any more than on a quarterly basis. Review your grant agreement to understand your specific reporting requirements. If your requirements are to submit reports on an annual basis, then your reports will be due 90 days after the reporting period. If you submit reports on an quarterly basis or semi-annual basis, then the reports are due 30 calendar days after the reporting period.

If in your reporting, you need to specify goals or costs and the goals were not met or the costs were greater than the budgeted amounts, you’ll need to explain. Be prepared to explain why goals were not met or why costs were overrun. With these few requirements which we provided, make sure the financial management system is equipped to handle and analyze variances between the budget and forecast and the actual results.

RECORD RETENTION AND ACCESS

Financial records, supporting documents, statistical record, and all other records associated with the federal award must be retained for at least 3 years after the final expenditure report is submitted to the federal awarding agency. There are times when the entity may need to retain the information longer than 3 years. If in the case there is any litigation, claim, or audit stated before the 3 years is completed, the information must be retained until the litigation, claim, or audit is complete. In addition, the entity is required to retain the information if the federal awarding entity requires the entity to do so.

In 2013 there was an executive order to make open and machine-readable the new default for government information. Therefore, the federal government states you should whenever practical to retain the data on machine- readable formats rather than closed formats or on paper. When allowing others to review the data, the following agencies must be given access: Federal awarding agency, inspectors general, comptroller general, and pass-through entity, or any of their authorized representatives. In addition, there is no expiration for the rights of access. Thus, as long as the records are retained these agencies and their respective representatives must have access.

FINAL THOUGHTS

We covered excellent ways in which to comply with the federal grant requirements. Are there more , certainly! If you would like to review the whole federal regulation click on this link. Remember to have a Financial Management System to record the financial transactions, budget, etc of the federal award. When you utilize technology, your administrative burden decreases and you can work on more productive tasks. Secondly, to assess if you comply with the requirements read the grant agreement and compare it to the entity’s internal control structure. Secondly, assess the risk of the entity not complying with the requirements of the agreement. When the entity needs to go out to bid, ensure the procedures are aligned with the uniform guidance as discussed earlier and ensure equipment and real property is secured and proper controls are in place to prevent loss, damages, or theft. And lastly, make sure the data is retained for at minimum three years from the last submitted report.

Do you think you are in compliant with the standards we covered in this report? If you are not, no worries. We can help! Call us today or email us at (408) 780-2236 or david@dfarnsworthcpa.com Another option is to familiarize yourself with the uniform guidance cost principles, grant agreement, and compare your entity’s internal controls to the grant agreement requirements. Good luck!

David Farnsworth, CPA

P.S. We are on a mission to help local governments with fraud prevention and governmental finance. We exist to help eliminate abuse, wasteful spending and fraud. Our goal is to help you run a transparent financially responsible District or Agency. When you’re ready, here are a few ways we can help right away:

- Sign-up to our monthly newsletter here. We cover topics ranging from fraud prevention, financial reporting, government budgeting, etc.

- Take our fraud risk assessment (link to assessment here) We’ll give you specific recommendations on how to improve your situation right away.

- Receive our free fraud prevention package (click this link to schedule a meeting)

- Jump on a video conference call to get specific fraud prevention recommendations (click this link to schedule a meeting).

- Request a proposal to perform the financial audit. request for proposal.

Great post.